The UK, once almost entirely reliant on coal-fired energy, had its first coal-free day since 1880 this month (Friday 21st April), meaning it is on schedule to be completely coal free by 2025. More coal-free days will depend on the availability of solar, especially in June and July. Approximately half the UK’s energy comes from gas, 30% from renewables and inter-country agreements, and the rest from nuclear.

Meanwhile in Thailand, the Electricity Generating Authority of Thailand (EGAT) is trying to build a further six coal plants and is complaining over the fact its 800 MW Krabi coal-fired plant has been temporarily shelved while its Environmental Health Impact Assessment is re-done, a process which is likely to take 18 months. EGAT is presently wringing its hands very publicly over how to plug this 800 MW hole in the energy security of Thailand.

Is the energy even needed? According to EGAT’s own report, dependable power-generation capacity in the South stands at 3,089 MW. Peak power demand in all 14 southern provinces reached 2,713 MW on June 28, 2016. Peak demand in the South is increasing by 5% per year. This means peak will exceed dependable-power generation some time in 2019.

This, on face value, would appear to be troubling. However, interconnectedness within Thailand is becoming more efficient. Upgrading the high-voltage transmission lines (HVTL) from the Central region could deliver hundreds of additional MW of energy. One HVTL extension from Prachuap Khiri Khan to Phuket is under construction and is expected to begin transmitting 650MW of energy by 2020. The South could be OK under this scheme into the 2020’s. Another planned HVTL line, from Phuket down to Hat Yai, Songkhla, will deliver an additional 1,000 MW by 2024. The main hitch is that the government’s Eastern Economic Corridor may need some of this energy, too.

What of national energy security, i.e., the idea you should be energy independent because of the fluctuations in the international energy market? Energy Minister Anantaporn Kanjanarat has made it clear that while buying energy from Malaysia is an option, Thailand’s energy generation should be 85-90% domestic by 2026 and 80-85% domestic by 2036, according to the national Power Development Plan 2015-2036 (PDP). However, at present only around 6.4% of Thailand’s energy is imported, mainly from Lao hydro. Another 800 MW is around 5% of EGAT’s total installed capacity of around 15,548 MW. So, relying on Malaysia is theoretically doable if peak power growth is really a problem, even if the ultranationalists complain about reliance on a foreign country.

The main obstacle is that Indonesia-Malaysia-Thailand Growth Triangle Project Development agreement, which controls the interconnectedness of electricity transmission, only covers 300 MW of energy from Malaysia to Thailand, an agreement which is mainly invoked when Myanmar’s gas blocks are shut down for maintenance. Boosting that 300 MW by another 500 MW to bring it up to 800 MW would require significant capital investment in Malaysia, which would have to be paid for by someone.

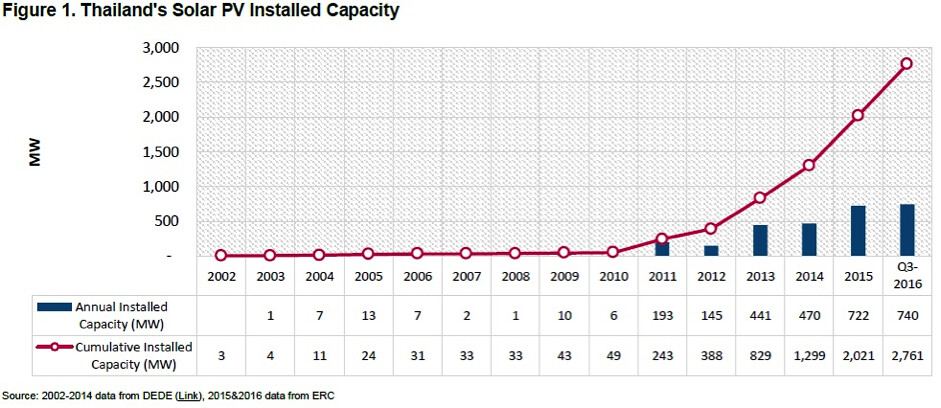

Now we turn to the elephant in the room, the one wearing photovoltaic panels. EGAT’s national PDP sees 6,000 MW of installed solar by 2036. This is, as everyone recognises, both pathetic and absolutely unreasonable, with a more realistic estimate being 8,600 MW by 2025. According to the PDP, installed solar as of 2014 was 1,298.5 MW. That means additional installed solar from 2015 to 2036 must average only 317.5 MW per year to come near 6,000 MW.

In fact, as of 2016, Thailand’s total installed capacity of solar was 2,753 MW, of which 2,623 MW was solar farms, the rest being solar rooftops. 2015 was a record year for Thailand’s solar, when an additional 722 MW was installed. So was 2016, with 740 MW+. You can see where this is going. The functionary who pulled the 6,000 MW figure out of the air should be forced to wear a baseball cap fitted with flexible photovoltaic panels illuminating a large neon sign above his head reading ‘National Energy Security Risk’. Actually, this German report, produced by the Renewable Energy Project Development Programme of the German Federal Ministry for Economic Affairs and Energy (BMWi), shows where solar in Thailand is going.

Yes, Thailand is adding over double what is predicted, with EGAT’s target of 6,000 MW likely to be broken by 2021, 15 years early, if around 700 MW is added each year. Is this likely? Well, yes and no. This is Thailand’s program for rolling out solar:

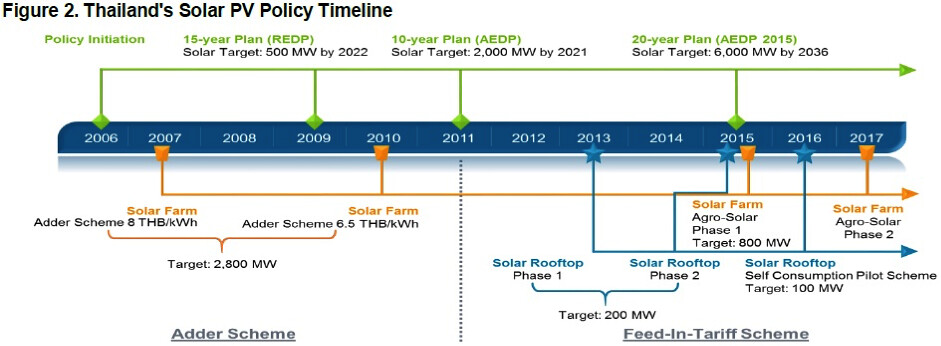

It basically consists of two programmes, solar farming and solar rooftop. There is a missing programme, commercial solar power plants, which is discussed later.

For solar farming, what is limiting deployment is a combination of government incompetence in licensing and a lack of feed-in tariff (FiT) compatible transmission lines, especially in the Northeast and South. This means things are progressing slowly.

In August 2014, the Government announced the “Governmental Agency and Agricultural Cooperatives Programme” (Agro-Solar programme) with an overall target of 800 MW. This programme aimed at realizing solar farms with a capacity of up to 5 MW in the form of public-private partnerships (PPP), with the governmental sector (Group 1, comprising governmental agencies, government-regulated universities, governmental organizations excluding state agencies and local administration units such as municipalities) and agricultural cooperatives (Group 2, including agricultural, land settlement and fishing cooperatives) as public partners.

However, the process was much drawn out, with the Energy Regulatory Commission (ERC) of the National Reform Council only publishing the details and regulations in March 2015, after the National Energy Policy Council’s approval. Following the approval, ERC announced the detailed application process on 17th September 2015.

The scheme is split up into 2 phases, and Phase 1 opened for application rounds in Nov-Dec 2015. However, due to difficulties fixing the selection criteria, the process was delayed, which shifted the scheduled commercial operation date of the projects to 31st December 2016. In Agro-Solar Phase 1, Group 1 projects were dropped because of complications in regulations managing PPPs, meaning the planned 600 MW were reduced to 300 MW. Moreover, there were difficulties with 200 MW of investments not being realised in 2016 because of predatory action by inactive investors, who sought to purchase the licenses and then resell them in a secondary market. Investor pre-screening has now been instituted.

Moreover, instead of transferring the 300 MW from Group 1 to Group 2 projects to make it back up to 600 MW, only 281 MW of proposals for Group 2 were accepted. None of these were in the Northeast or South because of the lack of infrastructure to manage FiTs. There is therefore a dire need for the infrastructure for FiTs to be developed in the South (and the Northeast) over the next three years. The government cannot simply say there is a problem with energy in the South without developing FiT compatible lines to stimulate decentralization and deregulation of solar energy in the region.

For the delayed Phase 2 of Agro-Solar, standing at 519 MW at a feed-in tariff rate of 5.66 baht/kWh over 25 years, a petition was filed by 2,000 agriculture cooperatives to drop embarrassing formalities of a lucky-draw style public tender by the Energy Policy and Planning Office. This delayed everything. Phase 2 should go ahead this year, though if the government regulations cannot be negotiated, only the 119 MW applicable to Group 2 will go ahead. Again, transferring the 400 MW applicable to Group 1 to Group 2 to make the total up to 519 MW seems not to have occurred to the government.

For solar rooftop, the first Thai solar PV rooftop FiT policy was announced in 2013, with a target of 100 MW for commercial (10-1,000 kW) and 100 MW of residential (0-10 kW) rooftop systems. The quota for commercial rooftop PV was rapidly attained, and the programme was closed. However, only approximately 21 MW of PPAs were signed in the residential sector. The systems were meant to be commercially operational by the beginning of 2014, but many were unable to even start until 2014 and 2015 due to licensing problems. As a response to the licensing problems, under the Quick Win Proposal by the Energy Reform Committee of the National Reform Council, solar rooftop licensing will now be streamlined, meaning there will be over 10,000 MW by 2036, with roughly 5,000 MW each from residential and commercial. This means the solar rooftop market alone has the potential to make Thailand’s 2036 target of 6,000 MW by 2036 seem laughable.

There is also the issue of commercial solar plants without government or agricultural cooperative partners. These range in the area of Very Small Power Producers (VSPPs), with a maximum of 10 MW and FiTs of 4.12 baht being considered for 2017 and 2018, to Small Power Producers, in the area of 10-90 MW. Thailand has no plans at present for plants over 100 MW, unlike in China, India, and the United States, which have many photo-voltaic solar power plants in the multiple hundreds of MW.

To make solar work in the south, Thailand needs deregulation and decentralization of the energy industry; the construction of FiT-compatible transmission lines; strong government encouragement, including streamlining licensing, i.e. cutting out the corruption, for agro-solar farms, VSPPs and SPPs; and a target of opening up the solar market for Medium Power Producers (approximately 100-300 MW) in the 2020s.

Solar, of course, is extremely national energy security-compliant. Thailand owns all the sunlight that falls on it. It passes General Prayuth’s ‘Pen khon Thai reu plao?” test with flying colors. As for coal, Thailand imported 11 million tonnes of extremely non-national energy security compliant coal in the first half of 2016 alone, mainly from Indonesia and Australia. So, here’s an idea. EGAT should just install the FiT infrastructure and then license 800 MW of a mix of solar agro, rooftop, and SPP specifically for the South over the next four years, using hybrid co-generating alternative energy power plants if necessary if the energy is expected to be firm, or always available.

Or, maybe the problem is that if this is done and is shown to be doable, people might wonder why the government is pushing ahead with the decidedly unpatriotic 2,400 MW Thepha coal-guzzling plant in Songkhla. Or any coal-fired power plants at all.

Prachatai English is an independent, non-profit news outlet committed to covering underreported issues in Thailand, especially about democratization and human rights, despite pressure from the authorities. Your support will ensure that we stay a professional media source and be able to meet the challenges and deliver in-depth reporting.

• Simple steps to support Prachatai English

1. Bank donation via the "Foundation for Community Educational Media (FCEM)", Krungthai Bank, account number 091-010-4328, Swift Code: KRTHTHBK

2. Or, Transfer money via Paypal, to e-mail address: [email protected], please leave a comment on the transaction as “For Prachatai English”